It seems that over a period of about 24 hours, HBD went on a wild ride. This was something that many were able to take advantage of, for great profit.

To those who were liquid and able to capitalize on the opportunity, congratulations. It is always good when markets present the chance to make money and people jump on it.

There is a big question, however. What does this say about HBD along with the potential pitfalls? It is something that we need to consider.

After all, if they can do it on the upside, with enough money, they can do it on the downside too. When something is dependent upon the market, it is susceptible to the same players.

Situations like these can help to focus attention on areas that fall short.

The Positives

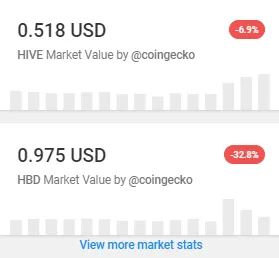

To start, we have to point out that things appear to have returned to normal. The price of HBD is back within a few points of the $1 peg. After pushing to $3, the price came crashing down.

Here is what we see now.

The internal exchange saw some enormous activity. This is a positive since the HBD stabilizer (along with many individuals) stepped up. The highlighted volume is an incredible increase over the norm. Typically, we might see $40K in trading on an average day.

At the time of this snapshot, the 24 hour volume was $1.3 million. Imagine if that was just an average day.

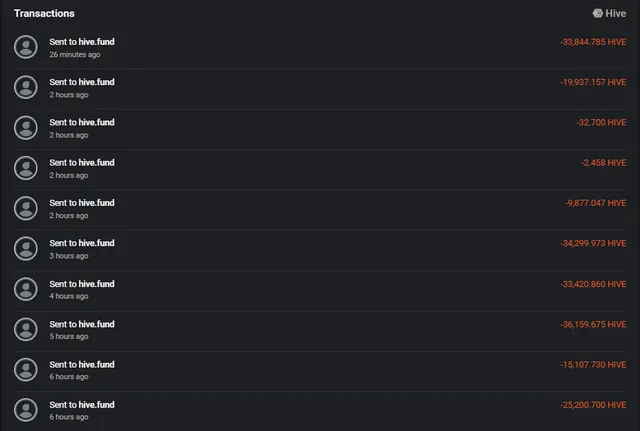

As a result of this, the Decentralized Hive Fund (DHF) was pumped full of Hive. The stabilizer was on a buying spree, directing the coins back to the DAO. As shown in a post by @tarazkp, the HBD Stabilizer was pumping in over 30K $HIVE into the DAO each hour.

This is money that will be used for funding further development over time. So, overall, we can consider that a net positive.

The Major Issue

Few are going to be surprised by the statement that a stablecoin should not see a 3x move. That is not the definition of stability. When we are dealing with volatility like that, even for a short period of time, we see how it is counterproductive.

Traders love spikes like that in currencies. Business people do not. If one is going to engage commercially, he or she does not want to wake up to a large move like this. Sure, some might say the HBD sitting in a wallet overnight was worth a lot more in the morning. That would be true.

However, what happens if they pull the same move, but this time on the down side? How would merchants feel about seeing their overnight sales reduced by 50% or more because the currency fluctuated?

That is not something they want. The same is true for any financial products tied to it. Over the last few months we discussed the idea of building derivatives tied to HBD. These mechanisms can operate as a hedge, reducing the risk associated with HBD. At the same time, they would be dependent upon it. Hence, a massive move in the stablecoin would equate to pricing of these other assets going haywire.

It is positive that, after a short spike, it does appear things are back to normal. Nevertheless, the pump in the first place is of concern.

This shows us we have a major vulnerability, at least in the short-term.

Liquidity

One of the obvious factors in this entire equation is the lack of liquidity. HBD does not have a large circulating supply which is them coupled by the fact that a fair amount of the free float is locked up.

This can be a double-edged sword.

Having a large percentage locked up is a benefit to the overall resiliency of the ecosystem We have to keep this in mind. Since each HBD is backed by $HIVE, those which are put into savings are not an immediate threat to the system. It requires going through the waiting period. Other ideas around time locked vaults could provide a similar benefit.

What this does affect is the liquidity of HBD on the open market. Since the circulating supply is low to begin with, especially after we deduct what is locked in the DHF, the situation gets compounded with it available in so few places. Here is where we are slapped in the face by reality.

The internal exchange along with Upbit are the two exchanges that can create a decent amount of volume for HBD. Upbit, naturally, is a closed exchange, only open to Koreans. So from a global perspective, this is a moot point. It is what allows the South Koreans to manipulate the coins so easily.

This leaves us with the derivative of HBD. Leofinance introduced $pHBD a few months back. Coincidentally (or not), they also introduced their BSC version, bHBD yesterday.

Having options is great. Nevertheless, adding pools is easy; having liquidity in them is another matter.

Some have mentioned the idea of developing automate market makers (AMM) as a solution. Perhaps that is the way to go but it is still turning to the same areas: the market.

Give People A Reason To Have HBD

At this point, HBD is entirely dependent upon traders (and bots). This is where the value comes from. As long as it is tied to the peg, by market forces, it is on par. However, beyond that, there is little incentive to be involved with HBD.

Here is where the shortcoming is truly exposed. It is also shines light on the directions we have to take.

To make HBD sustainable, we are going to need buildout in the area that gives HBD value, outside of market movements. In other words, people need a reason to have the coin.

Over most of this year, we covered this so we won't go too deep. However, we need to focus upon:

- liquidity

- depth

- infrastructure

- sophistication

This is what will separate HBD from many of the other stablecoins that are out there. At the moment, it is very crude, just like the rest of them. Developing financial products that move HBD out of this category is vital.

HBD is a process. The pump shows we rely exclusively upon the financial markets. Unfortunately, when you are dependent upon them, the scorpions can turn and sting you. This is the risk of dealing in this arena.

It is clear we still have a long way to go. The answer to liquidity is simply to give people are reason to have liquid HBD on hand.

And that comes from development.

If you found this article informative, please give an upvote and rehive.

gif by @doze

logo by @st8z