Continuing the deep dive into what decentralized autonomous organizations bring to the table, in Part Two of the series I will examine:

- the use of tokens

- tax responsibilities

- legal considerations.

In the Sources section, are a series of links to sites and articles, to help you with your own research.

To Token or Not To Token

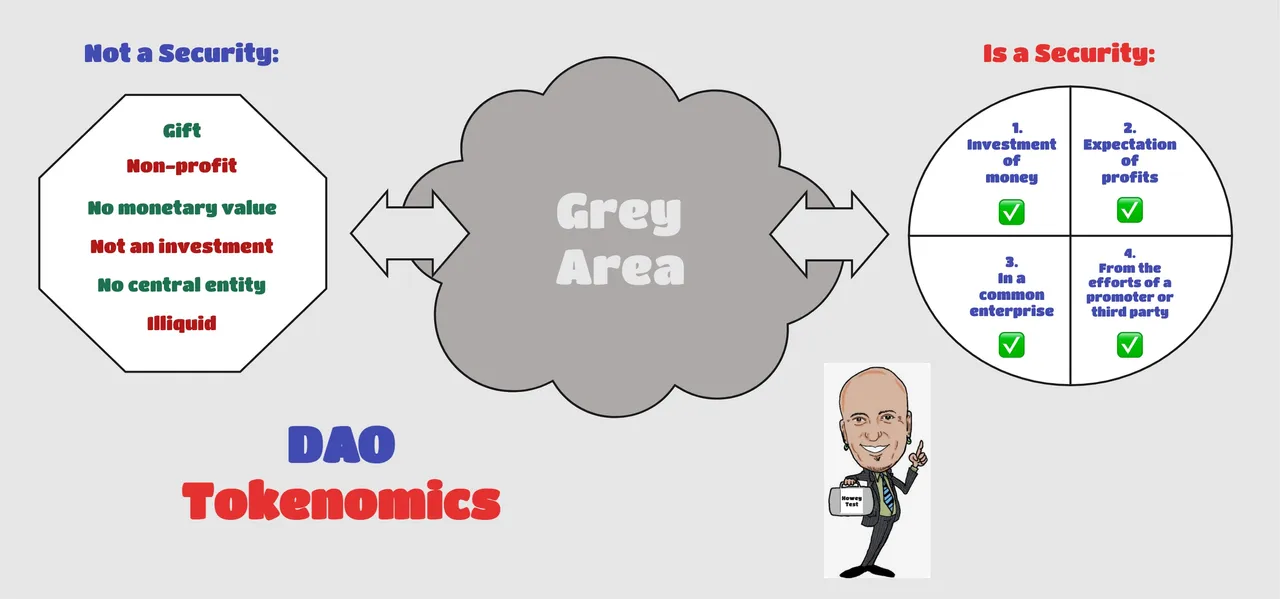

The technological advancements of decentralized autonomous organizations are moving at a much faster pace than centralized governments are able to establish regulations for their formation and ongoing operations. As a result, many founding groups are faced with large amounts of ambiguity when evaluating forming a DAO. One of those is whether to issue a token.

The major benefits of launching a financially oriented token for the DAO include:

- enable deposits for governance proposals

- enable voting on governance proposals

- building a treasury of funds

- create the means to stake and generate reward payments

- establish a way to financially interact with other DAOs

- enable a way to financially engage with DeFi protocols.

The primary concerns surrounding the issuance of these tokens by the DAO include:

- issuing, distributing, or selling of securities

- tax liability

- legal responsibility

- reporting requirements

- administrative and financial burdens, including costs.

However, tokens issued by the DAO do not have to be tradable tokens or carry a monetary value. They can simply be used for proposal and governance activities and distributed to members regularly or as needed. Tokens can also be issued as a form of access into the DAO, commonly referred to as token gating. This is especially common with non-fungible tokens (NFTs).

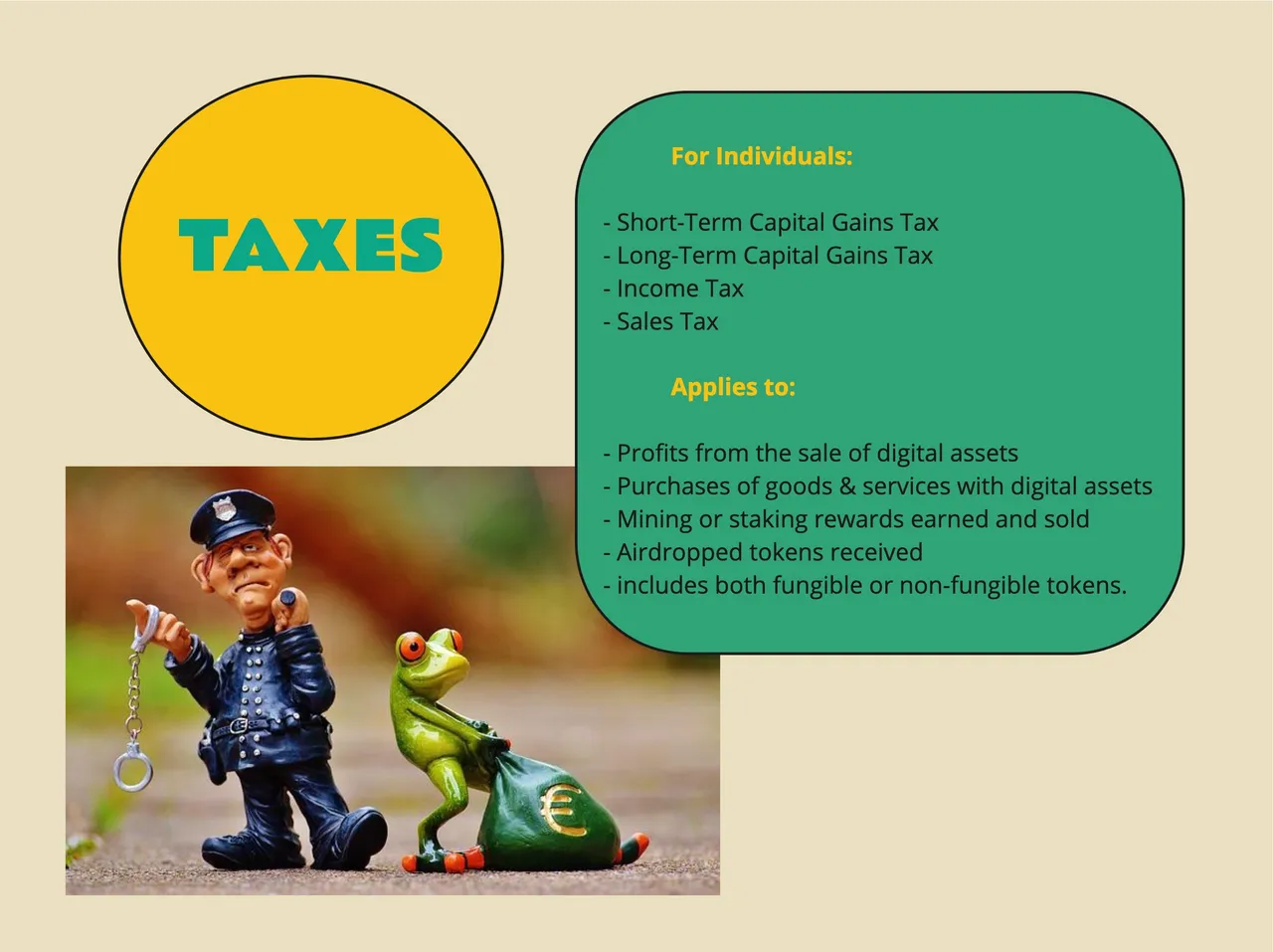

Tax Responsibilities

While specific tax rules and guidelines for DAOs are still under development, we have seen some guidelines emerge for members. For individual members in a DAO, this is what tax professionals agree on (from numerous published briefs, notes, bulletins, and articles on the subject):

- Rewards earned from DAO tokens will be subject to income tax.

- Profits made from the sale of DAO tokens will be subject to capital gains tax.

- Airdropped or other types of DAO token distributions will be treated as income, at their fair market value.

- You should keep detailed records of all transactions with the DAO, your share, and the profits made from the DAO.

Note that tokens in these cases refer to both fungible or non-fungible varieties.

As far as the DAO itself is concerned, there is little to no guidance available yet, when it comes to taxes. Again, it is reasonable to assume that DAOs will be treated as taxable entities going forward, when they can be classified as a group of participants or shareholders that work together to seek, earn, and divide profits.

Much of the above research is centered around guidelines in the United States and while many nations handle these matters in a similar fashion, it is important to evaluate international differences. In other words, do your own research in your country of residence!

Legal Considerations

Interacting with traditional businesses opens up a can of worms for DAO operators, including:

- opening a bank account

- establishing a mailing address (ex.: post office box)

- purchasing merchandise or services

- paying for expenses (ex.: travel and entertainment, supplies)

- paying wages to employees

- providing and paying for employee benefits

- executing a legal contract (ex.: office lease).

Let’s illustrate this with an example.

The DAO wants to participate at a conference and have members in attendance. Renting a booth will require payment in fiat currency, which will require having a bank account. Traditional banks will demand proof of legal status. Shipping booth displays and merchandise to the conference will again require payment for these services. Most convention centers have labor agreements in place and again these services will have to be paid for in fiat legal tender. While at the conference, DAO members are residing at hotels, eating at local restaurants, and using transportation services.

Alternatively, members can pay for expenses from their personal accounts and with personal credit cards; however, this will require reimbursement. In addition, as DAOs develop the need for hiring employees, paying employees, executing contracts, and entering into partnerships may arise. Again, a legal entity will be required to effectively handle these tasks.

Here is the key risk factor: if the DAO is not linked to a legal entity, it may make the members of the DAO liable for its debts! The DAO could be considered a general partnership by default, with the members being treated as general partners.

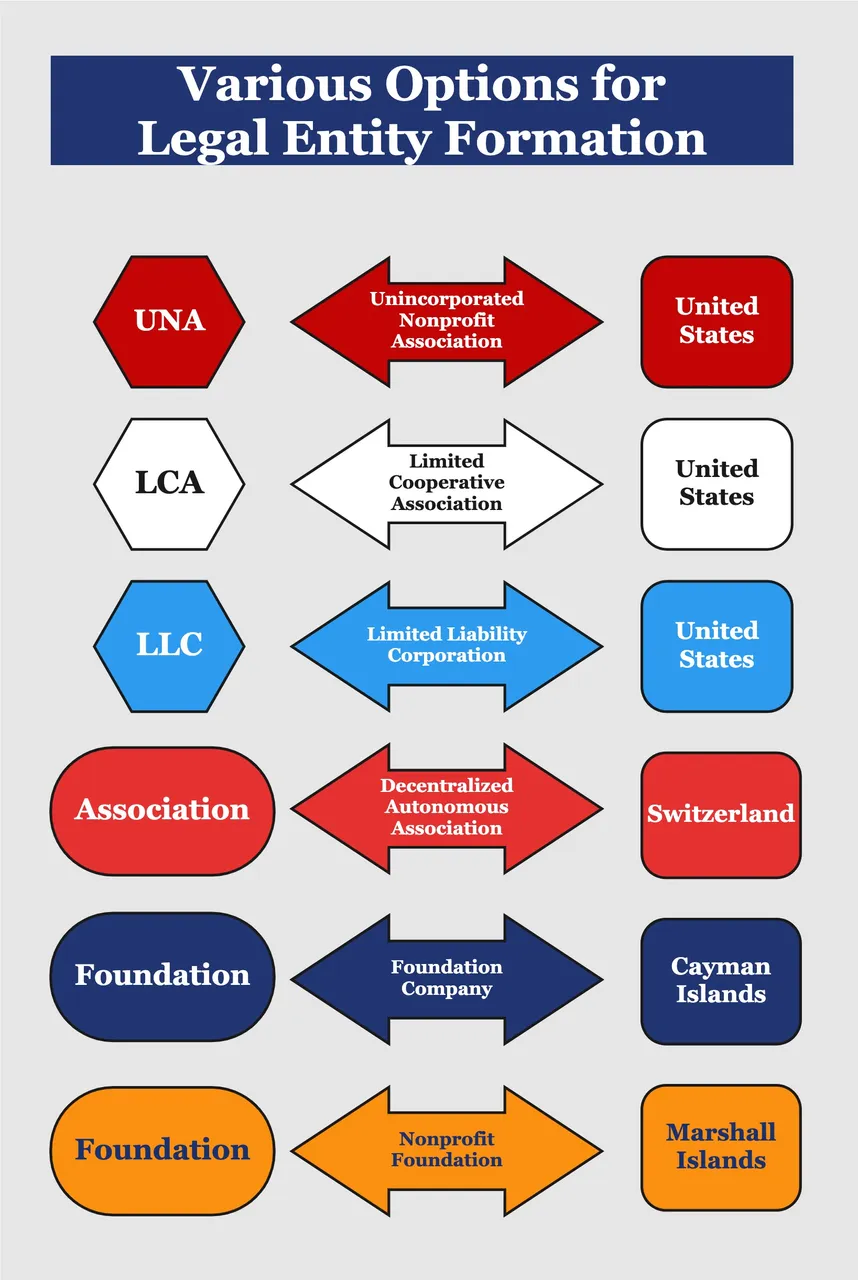

The States of Delaware, Wyoming, and Tennessee in the United States have established methods for the legal formation of a DAO, albeit as an additional delegation of the Limited Liability Corporation (LLC) or a type of LLC. With this, the DAO can operate as a legal business entity and interact with traditional businesses normally.

The earlier statement regarding international differences applies here, as well. For example, several options for registering as a legal entity exist as a DAO in the Marshall Islands, a Swiss Association in Switzerland, or a Cayman Foundation DAO in the Cayman Islands. In these cases, the DAO can be considered a non-profit organization.

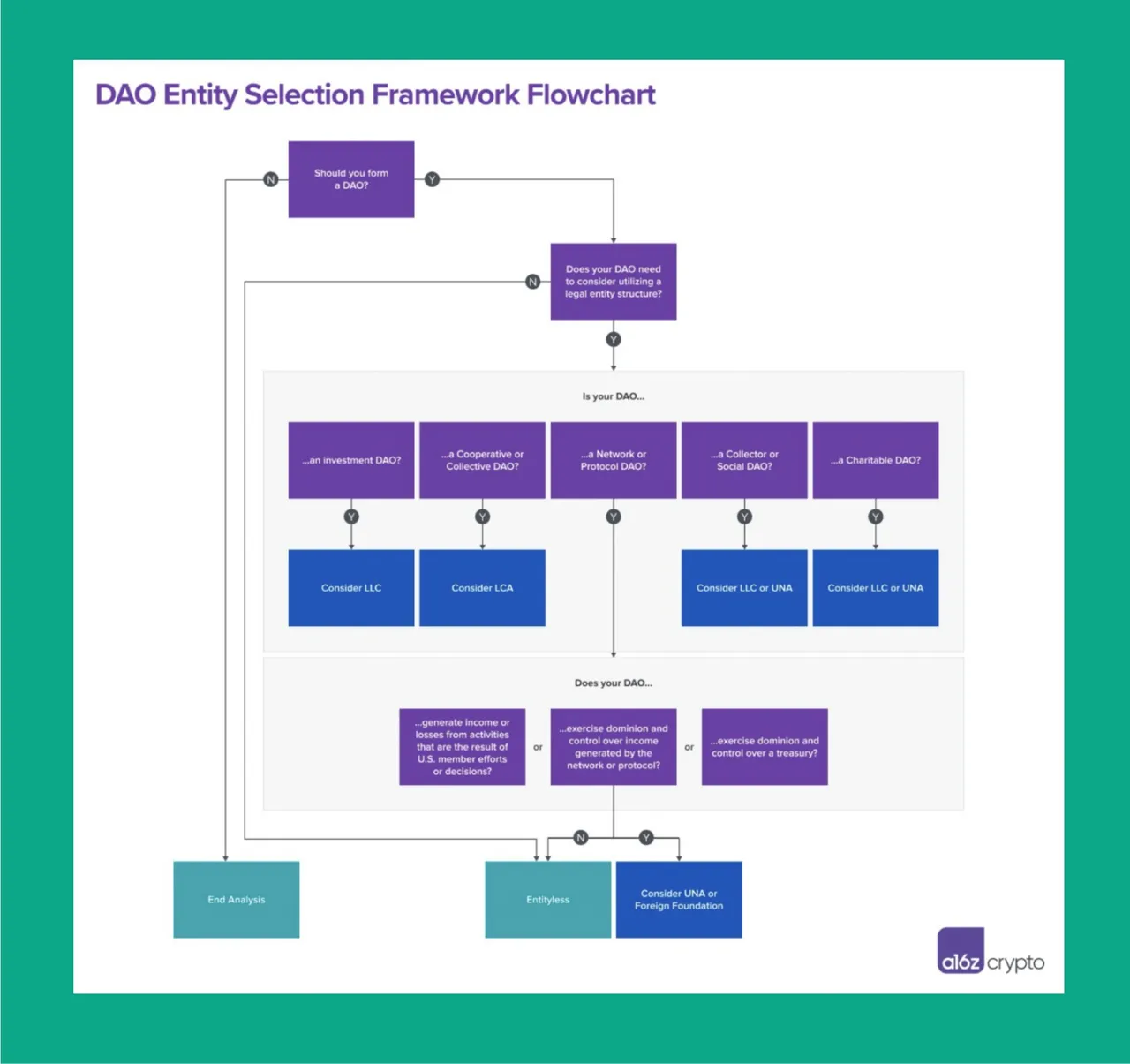

Whether members developing a DAO should consider establishing a legal entity structure is depicted by the flowchart pictured below. The flowchart was developed by a16z crypto and the entire article is in the Sources section.

Next Stop in our Journey of Discovery

Once we have established whether a token will be a part of the DAO and tax and legal responsibilities have been thoroughly reviewed and discussed with the founding members, the time has finally come to enter Web3 and establish a DAO. In the third and final installment of this series, I will examine some of the popular applications and tools used to build and launch a DAO.

Wordt vervolgd – Opa.

Sources, References, and Further Reading

Articles on Tokenomics:

From Florian -

https://medium.com/coinmonks/tokenomics-101-daos-f22dc516fa32

From Aragon - https://blog.aragon.org/incentive-design-tooling-for-daos/

Articles on Tax Responsibilities:

From TokenTax - https://tokentax.co/blog/crypto-taxes-for-daos

From TokenTax - https://tokentax.co/blog/nft-tax-guide

From CoinLedger - https://coinledger.io/blog/dao-taxes#:~:text=add%20for%20users.-,How%20do%20I%20pay%20taxes%20on%20my%20DAO%20taxes%3F,income%20and%20capital%20gains%20tax.

From Blockworks - https://blockworks.co/new-crypto-bill-suggests-some-daos-be-taxed-like-businesses/

Articles on Legal Considerations:

From Aragon - https://aragon.org/how-to/choose-a-legal-wrapper-for-your-dao

From the TN Bar Association - https://www.tba.org/?pg=Articles&blAction=showEntry&blogEntry=73474

State of Wyoming Information Sheet - https://sos.wyo.gov/Business/Docs/DAOs_FAQs.pdf

Delaware LLC FAQs -

https://revenue.delaware.gov/frequently-asked-questions/limited-liability-company-faqs/

Marshall Islands LLC Information -

https://www.offshorecompany.com/company/marshall-islands-llc/

From O’Melveny - https://www.omm.com/resources/alerts-and-publications/alerts/daos-looking-for-limited-liability-and-legal-personality/

From NoMoreTax - https://nomoretax.eu/legal-aspects-of-decentralized-autonomous-organisations-daos/

From a16z crypto -

https://a16zcrypto.com/dao-legal-entity-how-to-pick/

From a16z crypto - Legal Framework for DAOs Part 1

https://a16zcrypto.com/wp-content/uploads/2022/06/dao-legal-framework-part-1.pdf

From a16z crypto - Legal Framework for DAOs Part 2

https://a16zcrypto.com/wp-content/uploads/2022/06/dao-legal-framework-part-2.pdf

You can find me here:

Twitter - @KaasKop_Opa

Medium - https://medium.com/@KaasKop_Opa

Loop - https://www.loop.markets/user/52879

Leo Finance - @kaaskop