In the first two parts of this series we have explored the profit-driven waste mechanisms of our socio-economic system, but we have yet to talk about our contemporary monetary mechanisms - the foundation for so many of these problems we are witnessing today.

I will do my best to give a short summary of the history of money and how it eventually became "fiat money". It really is worth diving in deeper for those who haven't, but I want to keep this post relevant to the series, and whole books have been written just on fractional reserve banking alone.

For a deeper look I can recommend posts by @lucylin who has done some great articles on the concrete recent history of monetary manipulation. There are other great resources out there as well that go into the fine details, but considering the dry subject matter I will keep it as short and abstract as possible and try to drive home the core angles.

If you find reading about these things dull just choose a different format: scroll down and watch the amazing "American Dream" comic at the end of this post. It's a great starting point! Please also note that nothing here can or should replace your own research and understanding. We all make mistakes (including me), and only you can tell yourself what is true and what isn't.

Disclaimer finished ;)

A medium of exchange

We all know the story: One day long ago the idea came up that society could rely on a new tool for bartering and trading - a tool that would function as a valuable medium of exchange, but that would never in itself rot, spoil, or lose substance. A tool that could easily be transported, stored, counted and would - by its physical permanence - never degrade from its original value. Or that was the idea anyway...

Money was born.

A simple mind-hack put into the physical, to make trading and life in general way more convenient for all involved through the simple use of a placeholder of value.

It didn't take long for gold to become a medium of value exchange - through a social convention to regard it as universally valuable good that would always retain its value - and it would soon need securing against theft and unwanted access by people other than the actual owner as it became more frequently used by everyday people for barter.

Eventually, banks would start to establish themselves, granting the holders of gold a service in keeping it safe for them - in exchange for a fee. After all, this service was a valuable one to those who had too much gold on them than they could reliably protect and safeguard themselves, so the fee to them was 'warranted'.

And depending on who you ask, this is where the trouble really started.

Society was relying on these central places of value-storage more and more, and instead of getting their saved gold from the bank in order to pay for things they would soon start to use "placeholders" instead, issued directly by the banks. These "placeholders" came in the form of a piece of paper, guaranteeing that the holder of the paper will always be able to withdraw the amount printed on it in the form of actual gold they had originally deposited with their bank.

It was seen as a convenient way to guarantee your getting your valuables back from the vault whenever you chose to do so, and it had the welcomed side effect that a piece of paper is even easier to transport and store than gold (not to mention the actual tradeable goods that gold-currency was originally intended for).

In theory this all seemed rather convenient. However, soon it became apparent that there were some glaring issues with this development. People had neglected to notice that gold/money/currency in itself had already been the placeholder for value, but now these vouchers came in - effectively acting as paper placeholders for the old placeholders (gold).

Gold at least had intrinsic value because of its physical nature and its scarcity, and was therefore an acceptable placeholder for value to begin with. These vouchers however had no intrinsic value - other than the promise that they could be swapped for gold some day in the future.

Once you enter into such a voucher agreement, you would have to completely trust the bank to hold true to their promise that you could ever exchange the voucher back for "your" stored gold.

And nothing would necessarily prevent the bankers from leaving the bank closed one day - all their customers' gold stored inside it - and then running off with people's valuables, making people's voucher tokens worthless after a broken promise. After all, all they had given out to the people was this voucher which didn't hold any value in and of itself (other than making a fire with the paper), as opposed to a golden coin or a milk-giving cow representing actual value in the physical world.

But running off with all the people's money was not the only danger. The real threat to society came from the bad-intentioned idea to hand out more vouchers than the amount of actual gold stored in the vaults.

This seemed to be a rather smart idea from a profit-driven business perspective: If people use these vouchers all the time, hardly ever withdrawing their actual gold from the vaults, who would really notice if we handed out more vouchers than we have actual gold backing them? By doing this we could charge some extra fees and even offer people the deal that they could "borrow other people's money" for a while until they could pay it back. That way we could maximize the use of all this stored value in our bank, loaning it out to people who need it - for a profit.

And even loaning out more than we have actually stored...

And people dug the idea. Well, the "borrow other people's money" idea anyway. That fairy tale still holds up today. When you take out a loan you are NOT getting money other people put into the bank. Rather you are getting newly created money with immediate debt attached, calculated on the basis of existing reserves (if we can even trust that at this point).

It was now possible to get more money than you had, borrowing it from somewhere through the bank, allowing you to do what you needed to do. And at the end of the agreed timeframe you would pay back the money you had borrowed plus a little extra for the service of lending said money to you.

Thus, the concept of "interest" was born - an additional debt added to the original amount of money that was borrowed (the original amount loaned being called "the principal").

But this new model of banking had in turn some drastic malicious side effects as it spread. It became clear to those owning the banks that nobody could be certain that the amount borrowed in the form of vouchers was actually physically existent in the bank as reserve.

In other words unless you were a banker and directly bestowed with access to the vaults and books of the bank - you could never be certain how much gold was actually laying around in the bank for all the vouchers circulating out there.

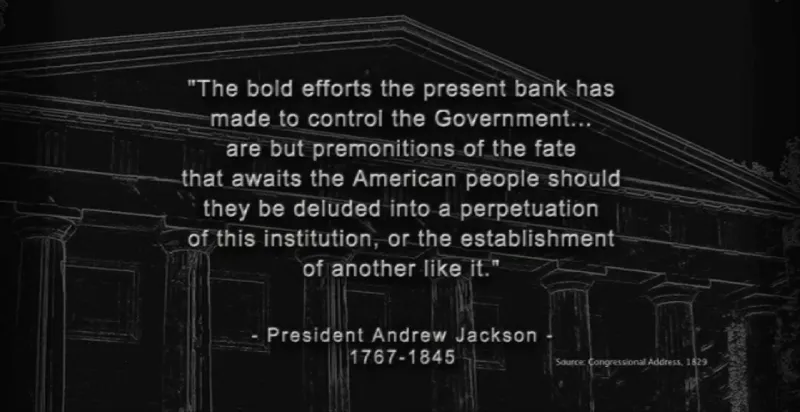

Thanks to the bankers' tireless promotion of this voucher model, people had gotten so used to the convenience and ease of using the bank's vouchers and their loan-services that the banks enjoyed an immense and ever-growing amount of trust. Governments and other authority systems had recognized the importance of the banks for the control of society very early on as well, and were already cooperating with the banks for their own interests.

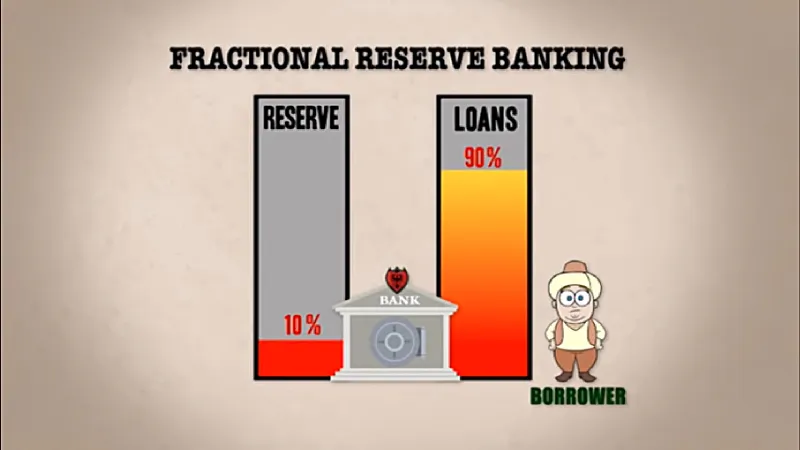

Eventually (and to make a long story short) the lingering idea of handing out more vouchers than were actually backed up in the vaults became the deciding business model for banks in most places around the world. This system (the same one we still "enjoy" today) is called the "fractional reserve banking system" simply because only a fraction of the supposed reserves need to be available in the bank in order for them to hand out loans. We have in effect decoupled money from its backing, and have made any insight and audit all but impossible, as banks are under no obligation to let us check their vaults for accuracy.

Instead we are in an obligatory position to trust them and their PR agents - whether we want to or not. They may call themselves "federal" or "national" but in almost all cases the central banks act as private cartels and not as public institutions. We fell for the packaging again.

I am confused, why is this such a problem?

There are several huge issues with this model of banking. First of all, if more money is loaned out to the public than is actually available at the bank to back it up, then a crisis-situation of political or social caliber might make people lose trust in their bank and end up with them wanting to withdraw their valuables from the bank.

But... if everyone tried this at the same time - there would not be enough gold and money to go around, despite everyone having originally deposited what they had. Because too much had been loaned out to other people unbeknownst to the depositors.

In other words if someone else took out a large loan, he would have gotten a temporary right to access a loan calculated on the reserves present. But not only that, because of fractional reserve banking the bank could hand out several of those loans to different people all referencing your deposit as the "reserve".

A rule of thumb is that about nine times as much money can over time be loaned out by banks to people for the amount that was originally deposited.

But because of the bank's interest fees demanded on TOP of the original loan, the individual taking out such a loan would always have to give the bank more money back than he had originally gotten from it. If you think "that seems fair, I mean the bank offered a service here" - you may want to reconsider. The problem with interest fees is that there will never be enough principal (money) in circulation to cover these interest fees, ever - because any new loan always comes with the extra interest-debt attached to it, and so does all the newly created money that could be used to ever pay back that first original loan. Talk about a circle-jerk!

We can make this simple in numbers with a fictional example of 10% interest.

I take out a loan for 10 gold coins (GC). The bank agrees and gives me 10 GC, but asks me to pay back 11 GC after the timeframe of - say - one year (10 GC principal + 1 GC interest). This means that I will have to come up with not only the actual amount I borrowed (principal) but also with that extra 1 GC the bank is charging me (interest).

The problem is that this one gold coin does not exist yet. The bank has effectively noted this extra gold coin for the future without having created it in physical form. But since it is now in the banks' books, this extra money DID come into existence - at least in the form of debt - a future liability to be paid regardless of availability. A debt that is not covered by the actual assets that exist currently.

This simple mechanism will show you that in a fractional reserve banking system there is ALWAYS going to be more debt than actual money in circulation, simply because any new money created automatically comes with new debt attached, to be paid back by some inexplicable method.

But: if the money for the interest doesn't exist in circulation, then where will I get it in order to pay back my interest fees?

And this is the crux:

You will need to take that extra gold coin... off of someone else.

You CAN'T be serious?!

I mean it quite literally. You will have to make sure that you get that extra 1 GC from another participant in society in one way or another. Translating this to the modern "economy" there are many examples of this. It's the status quo really.

Of course you could simply steal it from someone, which is frowned upon by society, might get you in trouble and might let your conscience weigh heavy on your heart.

But thankfully, we have all these "cool" new ways of stealing from others (including yourself) that don't get labeled as such. Instead they are called "solutions"... which don't really solve anything.

If you own a company: You could decide to not raise your workers' pay after the company has increased its profits. "Cutting that corner" will be more than enough to make up for the missing interest payments. For now. Heck, cutting corners is always great in a system where scarcity is rewarded (as outlined in Part 2 of this series).

Another way: You could sell things you own, just so someone would trade another GC of his with you voluntarily.

Or even better: you could keep all the material possessions you have and simply offer your services to someone, depending on what services you can perform.

Ideally this is something you want to do anyway, but more often than not it leads to some form of prostitution where people are "forced" to do something they would never do voluntarily just to come up with that "missing money" - be it outright prostitution or clandestine prostitution enjoying a different and more positive connotation in society.

Generally, all the things that people do MERELY because they are being paid for it qualify. I know, a suuuuper unpopular thing to say ;) But I bet all of us have gotten to know that feeling in depth, I sure know I have.

Now think about that for a moment: How many people in your life earn their 'missing payments' to the bank by doing something they hate? Many. If not most.

While it's true that most in society do not offer their sexual services to strangers, most in society DO offer their energy and lifetime to strangers and odd causes in one way or another just to cover the existing debts that come from a mathematical set of unnecessary parameters.

And whether we are talking about shuffling papers with numbers on them, sitting in a cubicle dealing with topics that don't interest you or whether we are talking about standing at a cash register accepting payments on behalf of the company you work for for the better part of the day - you are effectively giving away your time and life energy to be able to come up with the compensation for a systemic black hole that affects any- and everyone in society. A black hole that has no tangible or logical reason to exist at all other than to bind us to it, ruling the better part of Western civilization's affairs and daily worries.

You could of course also get that extra 1 GC back by simply taking out ANOTHER loan with the bank. Cool, you can now pay your old 1 GC debt back - high five!

But in effect you now have to pay the new loan interest back to the bank as well, which is even higher percentage-wise as before (because some of your new loan went to servicing the old debt payment and not to your immediate expenses).

While it may sound utterly insane to borrow more to keep paying off less and less old debts over time, that is precisely what we are all doing. Governments included.

Welcome to the "economy" of today. Move along, nothing to see here.

Hmm, but I don't see how interest can be such a huge issue...

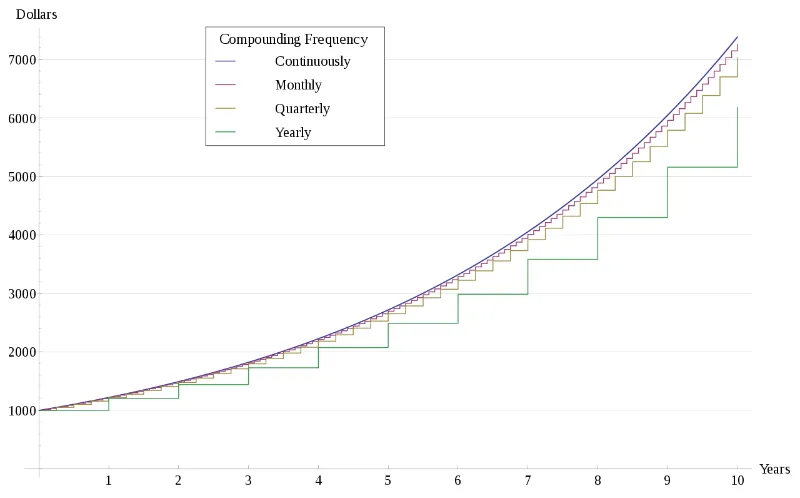

Well, the thing is that these effects add up greatly over time. Financial "experts" refer to this as "compound interest".

Although interest rates in our world are significantly lower than the 10% illustrated in the example above, you have to remember that the interest rates will be applied to your outstanding debt again and again as time goes on. And again. And again.

To our linear-thinking minds it is hard to comprehend what compound interest looks like and how quickly it can get out of control. After years or decades of not having paid off the loan (+interest) you end up paying the majority of your income to service the accumulated interest-debts only, not the actual principal you borrowed. That principal is still outstanding and will only start to diminish once you can pay in more money than the newly created interest charges you with.

The following graphic shows the effects of compound interest with a rate of 20%. The beginning stages are slow but then it blasts through the roof!

A great illustration of this is the act of buying a house today.

Now, to a thinking child the house would cost an amount of money equal to the materials, machines and people needed to build it.

Sounds logical, right? ;)

If you look around in actuality however you will see that houses are generally priced at several multiples of their original building costs. Who ends up "earning" the most when you buy a house? The construction firm? The mortar factory? The window guys?

It's the banks who loan you the funds... that earn the most when you buy a house through a loan.

Because the sum to build or buy a house is so large for the absolute majority of people the paying-off-duration will be quite long, during which compounding interest adds to your debt majorly over time until you end up having to pay - say - 500K for a house that originally required "mere" 110K to build. So in effect you are paying 3/4 to people who have never laid a brick on another, who have not spent weeks building the house for you, who have no idea how a house is built at all.

When you buy a house, most of the money goes to people in suits whose "only" job in this house-building process was to loan you a bit of their money for interest until you could pay them back. That is all.

Don't forget that until you pay in full, the companies involved have to in turn take out loans themselves, to pay for their workers, the material needed to start building the house, etc. Everyone in the economy is in need of funds constantly, and will often have to take out a loan before being able to get the payments from their customers after the project has been completed (which can sometimes take years or even decades).

Through this we can see how the overall effects of interest pile up in society, because interest is attached to any and all loans ever made, and the ones who took out this loan are systemically forced to get it back somewhere else, somehow.

It's called scarcity. But this scarcity has nothing to do with physical availability... and everything to do with a mathematical magic trick that is entirely unnecessary and that most people have not yet seen through.

The problem here is that this debt-enlarging mechanism does not only apply to you, me and other people - it affects all companies, institutions and even "countries".

And because more and more debt is added as new loans are taken out, the overall supply of money increases - in a futile attempt to cover the outstanding debts. We call this phenomenon "inflation". Inflation is simply the dilution of money's value due to an increase in its quantity. There are several differing analysis on inflation, but a conservative estimate seems to be that the US Dollar has lost about 96% of its original value since the founding of the FED - simply due to the constant increase in the amount of money in circulation (to cover existing debts).

Yikes!

What the media refers to as "national debt" is an entirely fictional and unwarranted debt, because it has been created purposefully by the very mechanism described above.

Only: now governments themselves are actually forced to steal from someone to cover THEIR 1 GC interest that they need to pay back on their loan of 10 GC because they agreed to a private cartel issuing the nation's money instead of themselves.

If that doesn't smell like conspiracy I really don't know what does.

And while many academically-minded people have protested when I put it as simple:

That is the whole reason for our financial deadlock. And for the constant shortage of money we all hear so much about.

The existence of interest attached to loans as immediate debt will ensure that there will always be more debt than funds to repay it. It's a crime, albeit a clandestine one that has still not been figured out by well-intentioned people doing their best to repay their debts. Daily.

The whole issue is that this was done on purpose, and it serves nicely to keep people in line and "occupied" instead of figuring out how they are being screwed.

If you hate to dwell on that notion, I feel ya!

In case you haven't seen my post on it, I highly suggest you start your search with the brilliant "American Dream" comic which gives a thoroughly entertaining rundown of this somewhat threatening subject matter, and explains the story much better than I ever could. It will leave you with a sense of positive vigilance, which is really all we need to re-evaluate one of the most unquestioningly accepted mechanisms of our times - "money".

Or to be more exact: Fiat money, created out of thin air to cover existing systemic debts.

Believe nothing, but understand as much as you can.

unsplash.com

unsplash.com

unsplash.com

Zeitgeist: Addendum

unsplash.com

The American Dream

Zeitgeist: Addendum

unsplash.com

unsplash.com

unsplash.com

unsplash.com

wikipedia.org

unsplash.com

Zeitgeist: Addendum

What I Learned in the Zeitgeist Movement - Prologue

1. Money Makes The World Go 'Round

2. Waste = Profit

Thanks for stopping by <3