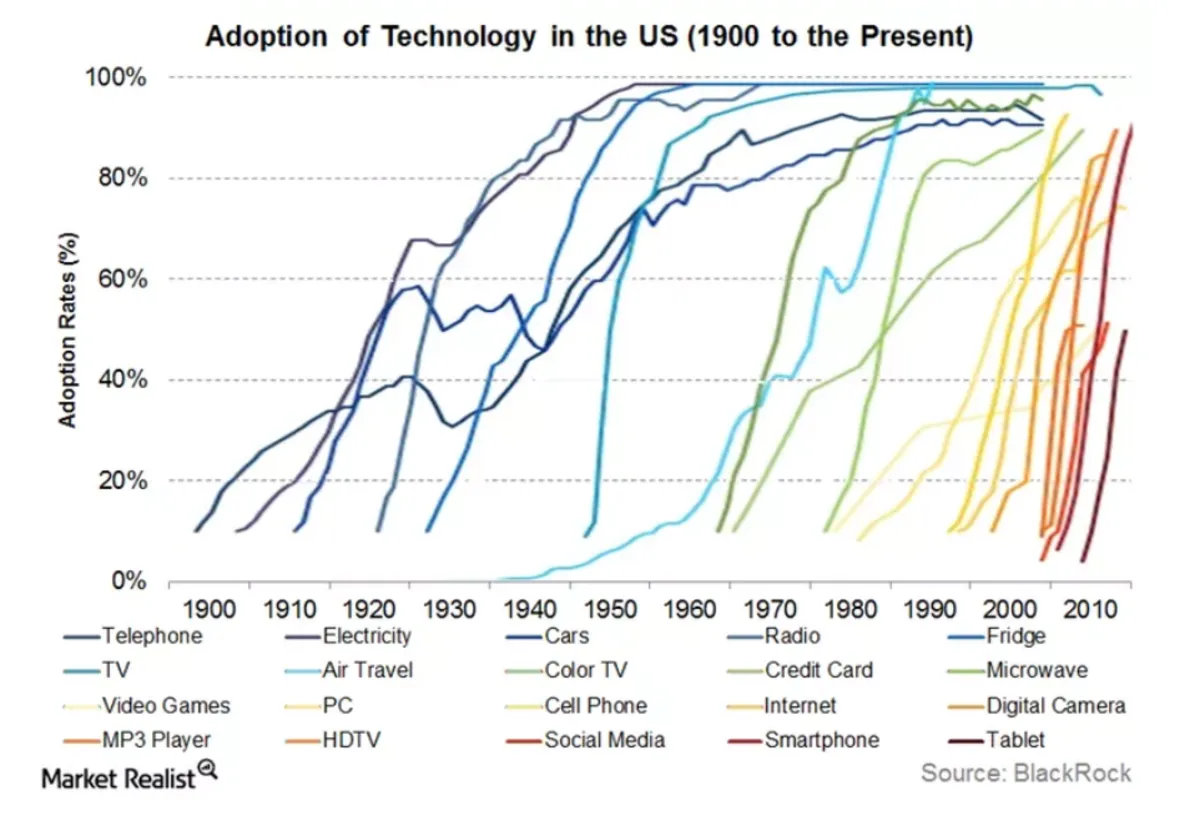

I read a very interesting analysis of the Power Law applied to BTC from @Edicted, and a chart of tech adoption sparked my interest. I am extremely biased towards tech advance, as my every post and comment reveals. I am convinced we're undergoing a fundamental transition, from centralized production requiring collective labor and management of hierarchies, to distributed and automated production requiring no labor that eliminates management and hierarchies, radically changing society permanently.

However, this transcendental transformation isn't the only consideration I have regarding my investments. I am also undergoing a transformation no less profound personally. Back in the 1980's this newfangled computer technology was transforming the world, and I plunged in with both feet, setting up my first network in 1987, becoming a computer consultant in the 90s, and being able to write a website entirely at a go in a text editor by the 00s. I was fully invested from my early adulthood to my middle age, and managed to prepare for my early retirement.

But I put all my eggs in one basket. Thinking I had finished playing the game, I prepared to senesce pleasantly tinkering in my shop and doing odd jobs in the nearby village, a bucolic dream that well suits my talents and bent. A concatenation of unanticipated events zeroed in on my assets like a laser guided missile, and suddenly just as I was retiring I found myself starting over from scratch without having any backup plan or reserve capital. Whoops!

Had I been 20 I'd have jumped on the bandwagon of the transformative technology of the day, then smartphones, and probably ended up coding Android apps, swapping shatter files, and bricking phones for a living, but at 50 my future looked a lot different than it did at 20. I didn't have 30 years to progress through a career, didn't have kids to raise, 2.3 dogs, and a fleet of trucks to feed and care for. I had my bags and tools my youngest had kept for me, my skills, and the network I'd built as a carpenter. Given that criminal corruption had been the primary vector of attack on my assets, I was pretty sour on assets that were vulnerable to corruption, and it didn't look like corruption was waning, either.

So, I pivoted to goodwill. I had a limited time to prepare for retirement (thank God I retired early and had that), and far more modest requirements than I did with a houseful of kids, dogs, and a four bay shop. I started innawoods, lived in a pickup truck and slept with my tools, graduated to a woodshed I remodeled into an off grid apartment, built a tool trailer with a cabin I could live on job sites in, invested in my network until I have ~50 clients that need odd jobs from time to time, and exchanged goodwill for an actual residence I didn't learn how to weld by making.

Retirement is the opposite trend of childhood, that part of a lifecycle BlackRock's chart doesn't show. As children we grow in stature, skill, and vigor, while senescence is the exact opposite. I had a heart attack 4 years ago, my back is trashed, and I shrink ~1mm every year. Holding a 16' 2x6 rafter free at a precise angle in one hand standing at the top of a ladder while I bury the nail with a hammer in the other hand is an entirely different job at 60 than it was at 40, and the bounce off the ground at the foot of the ladder is a lot more daunting than it was at 50. I'm more likely to hike my pants up to my nipples and snarl at the kids to get off my lawn than I am to swap mixtapes with them (or whatever the hell the kids are doing these days).

I'm about 80% in goodwill - that Citi can't swindle - and the balance in trade goods, tools, and cash (just in case of unforeseen and immediate needs). The goodwill I take with me when I die, and the rest is all rapidly settled by my heirs. No probate, inheritance taxes, or fights over fortunes will complicate my passing, because my boys got their inheritance when they moved out of my home. I don't need $1m to fund my lifestyle because it's not going to last that long. As your investments perform or fail remember that lightning never strikes the same person twice, because getting hit by lightning changes you, not because you can't get hit again. As you change, your investments should reflect those changes in you.