When we are faced with the possibility of investing our savings, the first aspect we look at is the interest rate, usually this is referred to as APY (Annual Percentage Yeld) or APR (Annual Percentage Rate).

In the world of cryptocurrencies, and particularly on Excange #Binance very often the APY is udsed for the staking DeFi, this percentage must not to be confused with APR.

Knowing these terms and their definitions accurately serves us to avoid wrong evaluations, and errors that could lead us to choose our financial product or to wrongly estimate our returns.

Let's see now the difference and what is the best way to estimate the earnings of our investment:

If we invest $1000 with APR rate of 5% and we get paid interest once a year, after one year we will have:

If instead the interest are paid every 3 months, every three months we have an accrued interest equal to

where n in this case is equal to 4, so a quarterly interest of:

From three months to three months our interest will be reinvested and revalued always with an APR of 5%, so we will have:

| Months | Interest | Total |

|---|---|---|

| 1 | 1000 x 0,0125 | 1012,5$ |

| 2 | 1012,5 x 0,0125 | 1025,16$ |

| 3 | 1025,16 x 0,0125 | 1037,97$ |

| 4 | 1037,97 x 0,0125 | 1050,94$ |

At the end of the year we will then find our wallet with something extra generated by compound interest which in this case is $0.94, the difference seems minimal, but over the years the interest itself will accrue by accumulation, and so the investment will rise in value exponentially over time.

This effect is even more evident if our investment included an accumulation plan or if the interest payment intervals were more frequent... But let's go step by step... 😁

If we look at the percentage of annual return on our investment, it will no longer be equal to 5%, but it will be higher because of compound interest (it's something like 5,004%), this new percentage calculated on an annual basis is called APY:

APY = Compounding Interest .

A practical example in the cryptocurrency world.

APY and APR interest rates in centralized finance are usually very low, if we want to invest by tying up an amount, we will usually have an annual interest that can range from 0.6 to 1.5%, we could hardly go beyond these figures.

More often than not, these percentages also need to be adjusted against bank or broker fees and charges that manage them.

On the other hand, in the cryptocurrency landscape we find projects of various types called Staking DeFi, which allow us to reach triple-digit APYs!

Now let me give you a rea example:

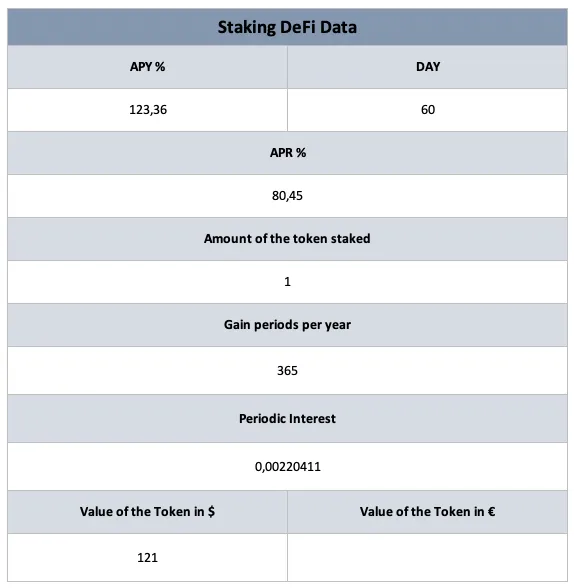

This very profitable DeFi staking generates an APY of 123.36%, the deposit is fixed for 60 days but I can at any time withdraw this investment.

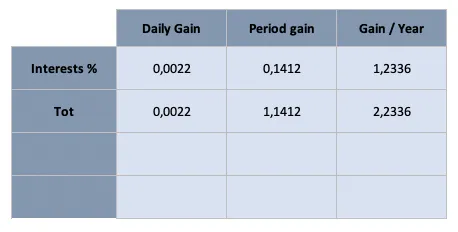

Another important information (which is not in the screenshot) is the interest accrual period: usually on DeFi staking proposed by #Binance the interest is accrued and paid once a day, this means that every day we will accrue, but this does not mean that we will make 123% every day, and we will not make a 123/365 every day, because APY takes into account the effect of compound interest.

We have to switch from APY to APR, which in this case is 80,45%.

This is the APY-APR converter you can use, but if you want you can also calculate it with Excel.

So putting 100 $ on this DeFi staking we will have after 60 days we will have:

As you can see by buying an AXS Token after the 60 day Staking period we will end up with 1.14 AXS, we will have earned 0.14 AXS which (at the time of writing this post) are worth about $18.06.

The values of APY are estimated and variable over time based on the performance of the project so when we are faced with the choice to invest we must be careful to:

- Carefully evaluate the project to which it relates;

- Use a small part of our personal capital.

Obviously when we are faced with double or triple digit APY our psychology leads us to bet, for fear of losing the train and for the desire to maximize our earnings.

In general I personally prefer to invest small amounts in many different projects rather than concentrate all resources on a single one (it is just like the risk of exposure of the stock market) never invest everything unbalancing on a single asset or a single market.

Conclusion

The cryptocurrency market and DeFi open up a universe of new opportunities in which we all have great possibilities for growth, the only really important variable is information, the one we read on dedicated websites, the one we find on crypto-socials like #Hive, and the one we share with friends who like us are fascinated by this evolving world.

Centralized finance is now old, it will share the next years market together with DeFi and other forms of innovative investment based on #value and #innovation.

Quando ci troviamo davanti alla possibilità di investire i nostri risparmi, il primo aspetto che guardiamo è il tasso di interesse, solitamente esso viene indicato come APY (Annual Percentage Yeld) o come APR (Annual Percentage Rate).

Nel mondo delle criptovalute, e in particolare sull'Excange Binance molto spesso viene fornito APY, che non è assolutamente da confondere con APR.

Conoscere bene questi termini e le loro definizioni ci serve a non commettere errori di valutazione che potrebbero indurci nella scelta di un prodotto finanziario sbagliato o nella stima sbagliata dei nostri rendimenti.

Vediamo ora la differenza e qual'è il modo migliore per preventivare i guadagni del nostro investimento:

Se investiamo 1000$ con tasso APR del 5% e ci vengono pagati gli interessi una volta all'anno, dopo un anno avremo:

Se invece ci venissero pagati gli interessi ogni 3 mesi, ogni tre mesi avremo un interesse maturato pari a

dove n in questo caso è pari a 4, quindi un interesse trimestrale del:

Di tre mesi in tre mesi il nostro interesse verrà reinvestito e rivalutato sempre con un APR del 5%, per cui avremo:

| Mesi | Interessi | Totale |

|---|---|---|

| 1 | 1000 x 0,0125 | 1012,5$ |

| 2 | 1012,5 x 0,0125 | 1025,16$ |

| 3 | 1025,16 x 0,0125 | 1037,97$ |

| 4 | 1037,97 x 0,0125 | 1050,94$ |

Alla fine dell'anno ci troveremo quindi con qualcosa in più generato dall'interesse composto che in questo caso è pari a 0,94$, la differenza sembra minima in questa cifra ma con gli anni gli interessi stessi matureranno interessi per accumulazione, e così l'investimento salirà di valore in maniera esponenziale in base al tempo.

Questo effetto è ancora più evidente se il nostro investimento prevedesse un piano di accumulo o se le periodicità di pagamento degli interessi fossero più frequenti... Ma andiamo per gradi... 😁

Se ora guardiamo la percentuale di rendimento annuo sul nostro investimento quest'ultima globalmente non sarà più uguale al 5%, ma sarà più elevata per via degli interessi composti (qualcosa come 5,004%), questa nuova percentuale calcolata su base annuale prende il nome di APY.

Un esempio pratico nel mondo delle criptovalute

I tassi di interesse APY e APR nella finanza centralizzata sono in genere molto bassi, se vogliamo investire vincolando una cifra, di solito avremo un interesse annuale che può andare dallo 0,6 al 1,5%, difficilmente potremmo andare oltre queste cifre.

Spesso inoltre tali percentuali devono anche essere corrette rispetto alle spese e alle commissioni bancarie o dei broker che le gestiscono.

Nel panorama delle criptovalute invece troviamo progetti di vario tipo chiamati Staking DeFi, che permettono di raggiungere APY a tre cifre!

Ora vi faccio un esempio reale:

Questo staking DeFi molto remunerativo genera un APY pari al 123,36%, il deposito è vincolato a 60 giorni ma posso in ogni momento ritirare questo investimento.

Un' altra informazione importante (che però non c'è nello screenshot è il periodo di maturazione degli interessi che solitamente sugli staking DeFi proposti da #Binance gli interessi vengono maturati e pagati 1 volta al giorno, questo vuol dire che ogni giorno matureremo, questo però non vuol dire che matureremo 123% ogni giorno, e neanche che matureremo 123/365 oni giorno perchè appunto APY tiene conto dell'effetto dell'interesse composto.

Dobbiamo passare da APY a APR, che in questo caso è pari all'80,45%

Questo è il convertitore APY-APR che potete utilizzare, ma volendo si può anche calcolare con Excel.

Quindi mettendo 100 euro su questo staking DeFi avremo dopo 60 giorni avremo:

Come potete vedere comprando un Token AXS dop il periodo di Staking di 60 giorni ci ritroveremo con 1,14 AXS, avremo guadagnato 0,14 AXS che (al momento della scrittura del post) valgono circa 18,06$.

I valori di APY sono stimati e variabili nel tempo in base all'andamento del progetto quindi, quando ci troviamo davanti alla scelta di investire dobbiamo stare attenti a:

- Valutare con attenzione il progetto a cui si riferisce;

- Utilizzare una piccola parte del nostro capitale personale.

Ovviamente quando siamo davanti ad APY a due o a tre cifre la nostra psicologia ci porta a scommettere, per paura di perdere il treno e per voglia di massimizzare i nostri guadagni.

In genere io personalmente preferisco investire piccole cifre in tanti progetti diversi piuttosto che concentrare tutte le risorse su un progetto unico (è proprio come il rischio di esposizione del mercato azionario) mai investire tutto sbilanciandosi su un solo asset o su un solo mercato.

Conclusione

Il mercato delle criptovalute e la DeFi ci aprono un universo di nuove opportunità in cui tutti abbiamo grandi possibilità di crescita, l'unica variabile veramente importante è l'informazione, quella che leggiamo sui siti internet dedicati, quella che si trova sui cripto-social come #Hive, e quella che condividiamo assieme agli amici che come noi sono affascinati da questo mondo in piena evoluzione.

La finanza centralizzata è ormai vecchia, essa condividerà il mercato dei prossimi anni assieme alla DeFi e alle altre forme di investimento innovativo basate sul #valore e sull'#innovazione.