Theory

The exponential moving average differs from the simple moving average in that more recent samples are more strongly weighted. This means that the exponential moving average responds more quickly to changes in the signal.

Implementation

The signal parameter is a one dimensional array. the smoothing parameter controls how much influence the more recent samples have on the value of the average.

import numpy as np

def exponential_moving_average(signal, points, smoothing=2):

"""

Calculate the N-point exponential moving average of a signal

Inputs:

signal: numpy array - A sequence of price points in time

points: int - The size of the moving average

smoothing: float - The smoothing factor

Outputs:

ma: numpy array - The moving average at each point in the signal

"""

weight = smoothing / (points + 1)

ema = np.zeros(len(signal))

ema[0] = signal[0]

for i in range(1, len(signal)):

ema[i] = (signal[i] * weight) + (ema[i - 1] * (1 - weight))

return ema

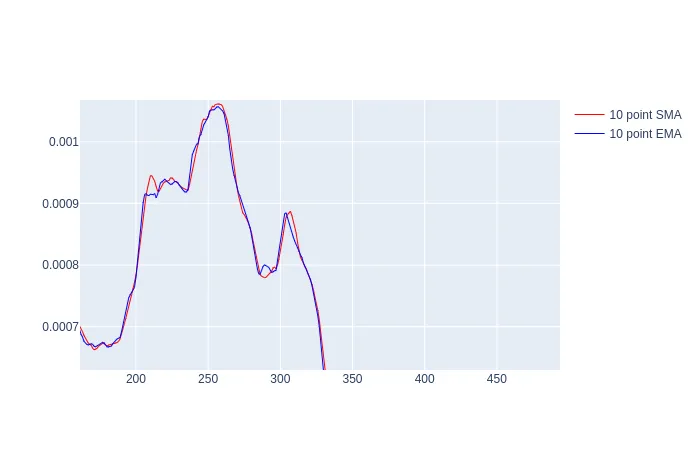

Results

Consider the following diagram showing the exponential average in blue and the simple average in red. Note that the exponential average leads the simple average, reacting to price changes more quickly.