Warning:

This post is quite theoretical and might be difficult reading for some readers who do not have a background in economics or mathematics. I have tried to explain the concepts as simply as possible. Demand and supply are important concepts to be aware of in order to understand some of my other posts which contain applied economic subject matter.

The section of the post relating to equilibrium is the most important part of this post. The problems with equilibrium is not typically discussed in much detail by economists and is worth a read if you want to know more.

Demand, supply and equilibrium are considered by many economists as the backbone of economics. Almost everything relating to economics somehow finds its way back to demand, supply and equilibrium. So what are demand, supply and equilibrium? Are they as critical to economics as many economists claim they are?

What is demand?

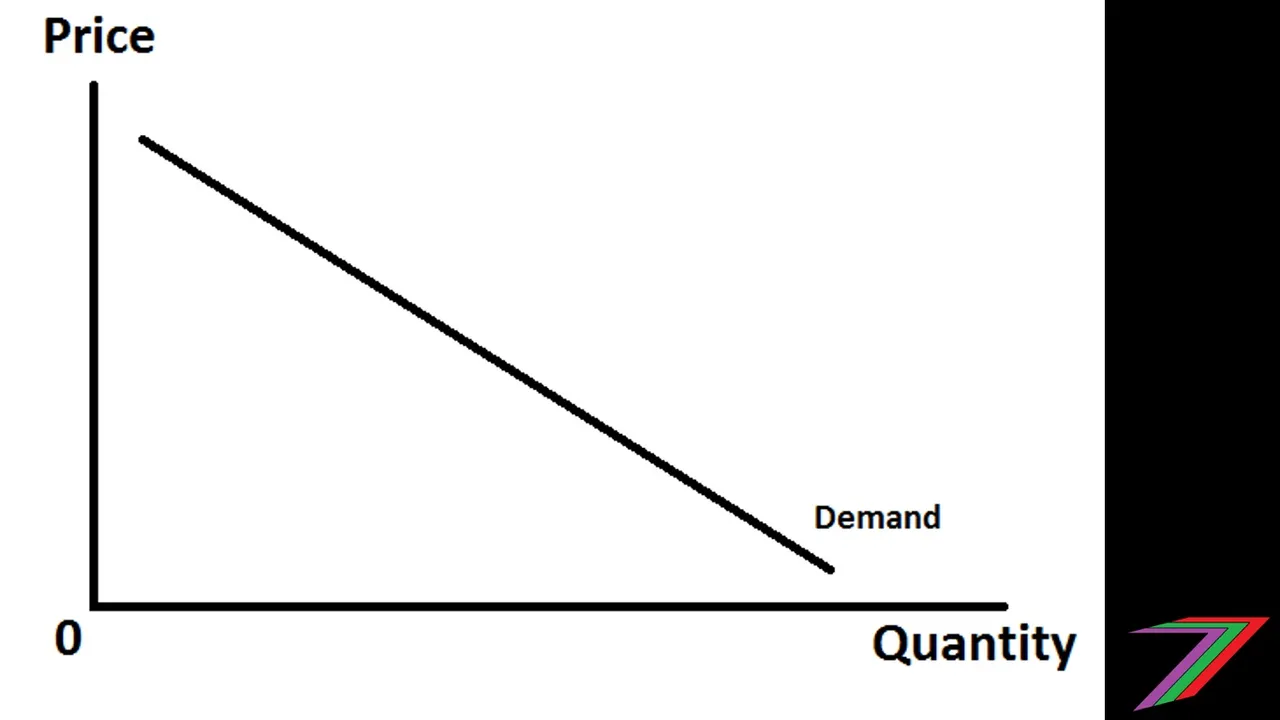

There are few ways of looking at demand. You can look at demand from the individual’s perspective or you could look at demand from the market perspective. An individual’s demand can be summarised as that person’s willingness and ability to pay. A person’s demand can be expressed mathematically and graphically. A reverse demand equation (it is called ‘reverse’ as price is the subject of the equation rather than quantity demanded) can be expressed as follows:

Price = α – (β × Quantity demanded)

The equation consists of parameters and variables, α and β are parameters and price and quantity are variables. For the above reverse demand function, price is the subject of the equation. Price is dependent on parameters α and β, and quantity demanded. α is the maximum a person is willing and able to pay and β is the sensitivity of price to a change in quantity demanded. What this means is that this person will never pay more than $α. The person will decrease their quantity demanded by 1 unit for every $β increase in price. For example, if a jar of peanut butter costs $4, Jack buys 3 jars. If the price increased to $5, Jack buys only 2 jars; β has a value of 1 for Jack’s demand function for peanut butter. This equation can represented graphically as shown below.

Demand curves (it is called a curve but for simplicity it is often drawn as a straight line) are typically downward sloping. When price increases people will buy less. When price decreases people will buy more. There are many factors other than price that influence demand. I will not cover these today.

What is Supply?

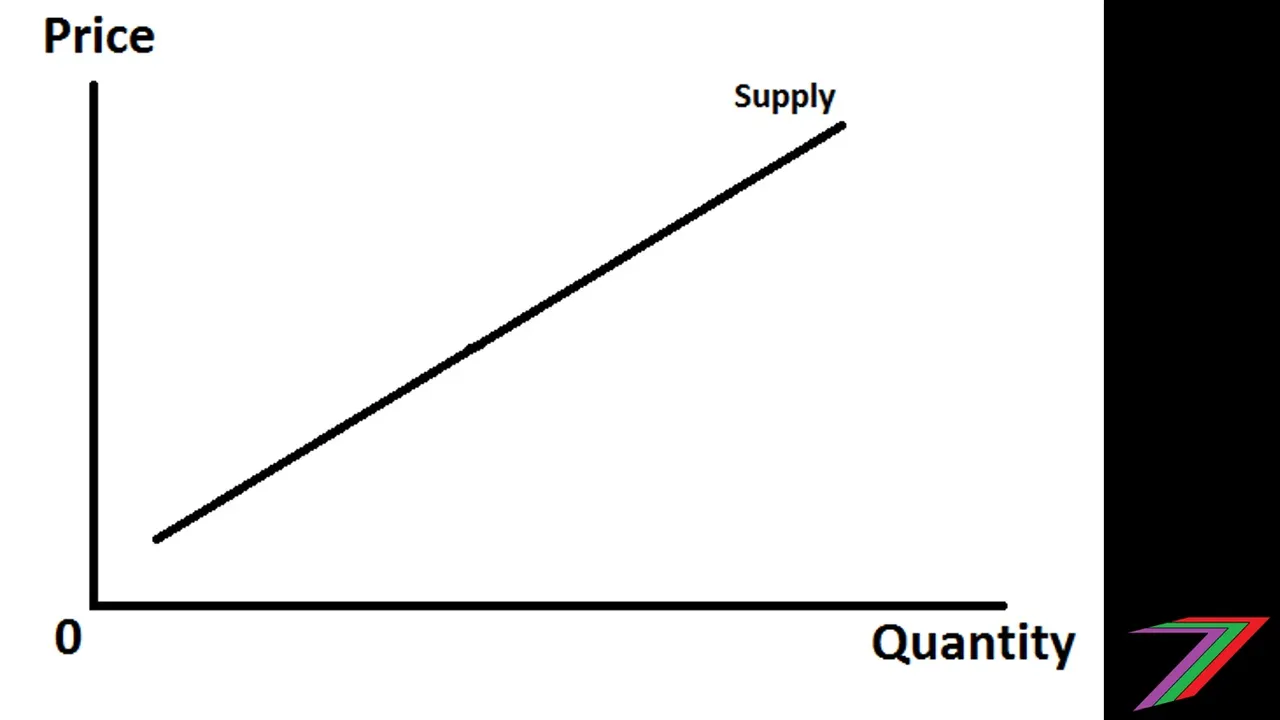

Supply is the output generated by a firm or firms. Supply is typically driven by market price and costs of production. In this post, like with demand, I will focus on price. Supply, like demand, can be represented mathematically and graphically. A supply equation can be expressed as follows:

Price = γ + (δ × Quantity supplied)

Price is dependent on parameters γ and δ, and quantity supplied. γ is the minimum price a firm requires to begin production and δ is the sensitivity of price to a change in quantity supplied. Both parameters are typically positive. Firms generally require a price above $0 to commence production and as price increases firms will increase production. These statements assume that price and quantity supplied are the only variables that change. This what we call ‘Ceteris Paribus” in economics. For today, that is all we need to know. Quantity supplied can be represented graphically as shown below.

Supply curves are typically upward sloping as higher prices encourage increased production. Like with demand, there are many other factors that influence quantity supplied. For the purpose of this post, we are only concerned with price.

What is Equilibrium?

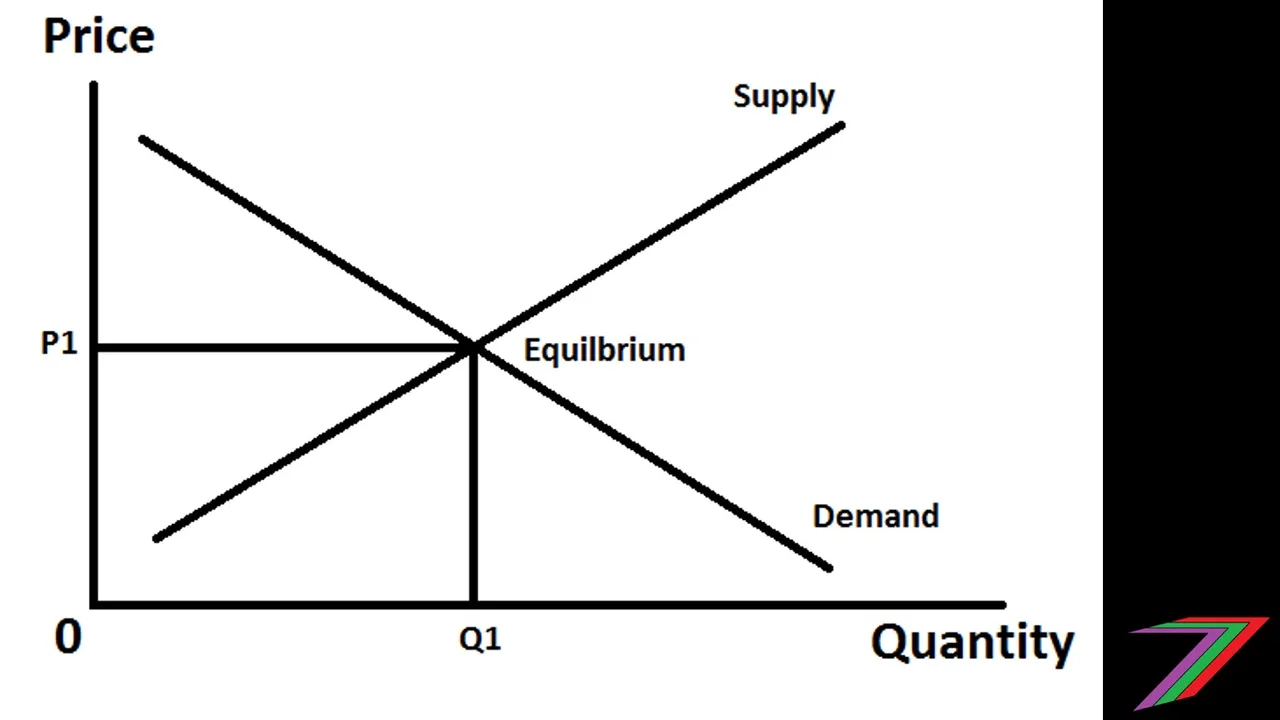

Equilibrium is the market price and quantity of goods and services sold when demand equals supply. Equilibrium can be represented both mathematically and graphically. Equilibrium can be expressed as follows using the demand and supply functions described above:

Equilibrium Quantity = (α - γ) / (β + δ)

Equilibrium quantity can be easily determined mathematically by solving the demand and supply function simultaneously. Price can be determined by inserting the equilibrium quantities into the demand and supply functions. If mathematics is not your thing. Equilibrium can be demonstrated graphically as shown below.

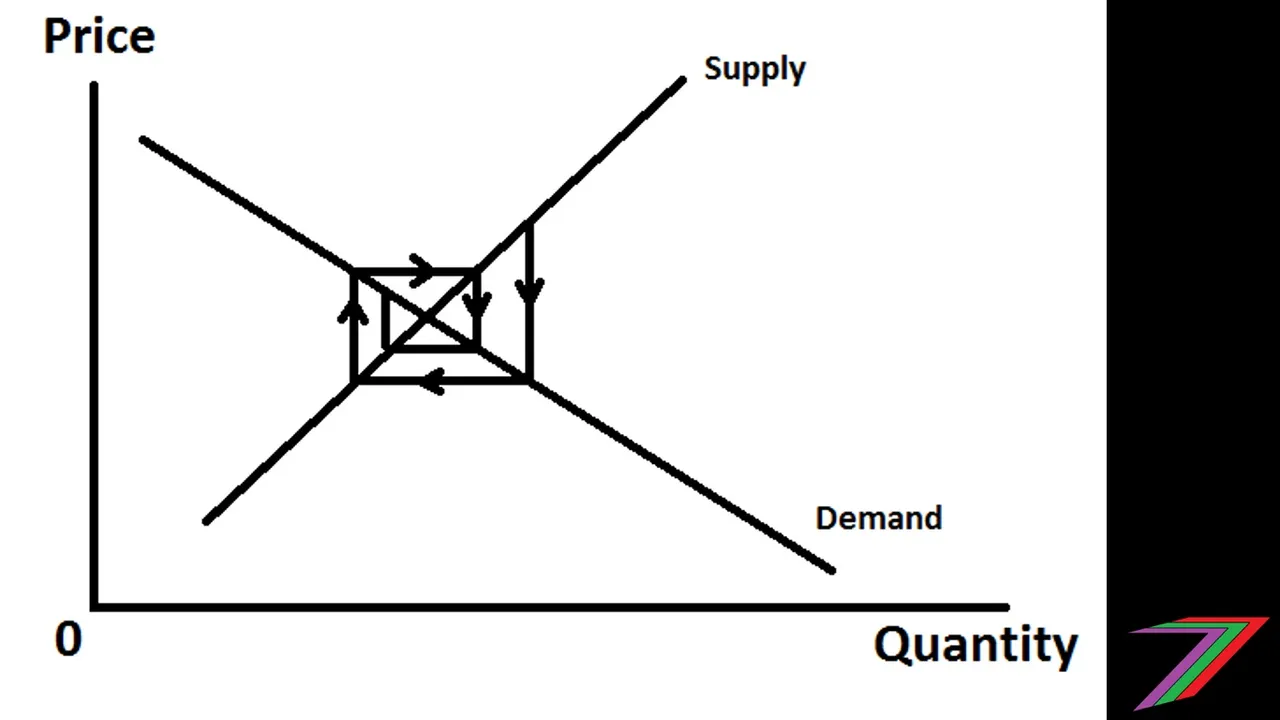

Is equilibrium ever reached? That is impossible to know for sure as the world is constantly changing. Also, suppliers do not know people’s demand functions and people do not know supplier’s supply functions. Simply put, it is highly unlikely we will ever reach equilibrium. If we do, it will be a pure coincidence and will only last a short period of time. Even if we assume the world is not constantly changing, determining and understanding each other’s preferences and costs takes time. The simple cobweb model below demonstrates how an equilibrium could be established in an unrealistic static world.

Even this model requires that suppliers are more sensitive to price changes than buyers, otherwise the cobweb does not converge to an equilibrium. In short, equilibrium price and quantity cannot be determined in the real world.

Another fundamental problem with determining equilibrium as described in this post is that this type of equilibrium is known as a ‘partial equilibrium’. A partial equilibrium means that the good or service being analysed is looked at in isolation. Other goods and services that might be complementary, substitutional or in some way indirectly influence decisions relating to the good or service being analysed are ignored.

For more information on substitutes and complements please read my post at the following link: https://steemit.com/economics/@spectrumecons/economic-concepts-3-substitutes-vs-complements. I will have another post describing general equilibrium and how it differs from partial equilibrium.

Should demand, supply, and equilibrium be considered the backbone of economics?

It is important to understand the basic relationship between price, quantity demanded and quantity supplied (all other factors held constant “Ceteris Paribus”). Attempting to determine equilibrium using demand and supply is pointless. Understanding that demand and supply influences price and quantity is a more practical application when considering free markets (minimal or no intervention from Government).

Getting back to the question, should demand, supply, and equilibrium be considered the backbone of economics? My answer has to be, no. There are many important factors that influence both demand and supply, none of which I have discussed in this post. These factors should form the backbone of economics. Demand and supply is just one way of representing these factors.

I will discuss these other factors in posts to come. I will not leave you all hanging, some of the factors that I consider more fundamental to economics than demand and supply are as follows:

- Utility (satisfaction and happiness of all, not just related to consumerism or even limited to human beings).

- Perception (individual and group, what influences our perceptions of the world and in turn how we act upon those perceptions).

- Efficiency (how to get the most out of what we have, not necessarily linked to production and output).

- Choice (what influences our behaviour and the decisions we make, strongly influenced by our perceptions).

- Ownership of factors of production (fundamental cause of poverty and scarcity, this is an area I wish we did not to focus on).

This list is not exhaustive but it is just to give you an idea of what I believe needs to be focused on in economics. I have not included scarcity on the list. I believe scarcity is predominantly contrived and links back to ‘ownership of factors of production’. For about information about scarcity. Here are the links to the first four parts of the series.

Scarcity (Part 1)

https://steemit.com/economics/@spectrumecons/scarcity-part-1

Scarcity (Part 2)

https://steemit.com/economics/@spectrumecons/scarcity-part-2-natural-or-contrived

Scarcity (Part 3)

https://steemit.com/economics/@spectrumecons/scarcity-part-3-meat-and-dairy-land-use

Scarcity (Part 4)

https://steemit.com/economics/@spectrumecons/scarcity-part-4-labour-capital-and-entrepreneurship

Scarcity (Part 5) will be posted in the weeks to come.

Conclusion

This post is fundamentally theoretical and fundamentally mainstream in regards to the treatment and explanation of demand and supply. This could understandably be difficult reading for those not familiar with economic concepts. For this, I apologise to my non-economist readers. The section on equilibrium should be the main take away from this post. I will just quickly summarise the problems with using demand and supply to determine equilibrium price and quantity.

- Buyers are not aware of supplier cost structures.

- Suppliers have limited knowledge of buyer preferences and intrinsic value for goods and services.

- Demand and supply can only be used to determine a ‘partial equilibrium’. Prices of alternative services and goods, which could be complements and substitutes, are not considered.

- There are many more factors that influence quantity demanded other than price. These factors could be:

o changing tastes

o changes to technology

o changes to income and wealth

o changes to efficiency and productivity

o availability of resources

o changes in laws and regulations

o and many others

I would like to thank you all for taking the time to read this post. I will have more economic concept posts to come.