The biggest innovation of DeCus is the use of overlapping grouping algorithms, which can make the custodians’ collateral less than the assets under custody.

DeFi is an eternal hot spot in the cryptocurrency market.

Since its emergence, DeFi has created multiple waves in the cryptocurrency market.

The first wave, in the second half of 2019, was when the concept of DeFi was proposed, and the Staking economy exploded. Since then, various imitations of “Staking” have appeared.

The second wave, in June 2020, was when COMP, the lending platform, started the liquidity mining and DeFi became a hot spot once again.

In the third wave, in July 2020, AMPL pushed the concept of an algorithmic stable coin to a climax.

The fourth wave was in September 2020, with YFI and SushiSwap. The former being an aggregated yields farming platform and the latter launching the market-making mining.

The fifth wave, in March 2021, saw Uniswap and SushiSwap bring DEX and liquidity mining to the forefront again.

But DeFi’s innovation is far from over…

Rigid demand: cross-chain BTC

Before DeFi, each public chain went its own way, whether it was for payment settlement, games, or other types of applications, each used its own independent ecosystem on their corresponding public chain. However, after the rise of DeFi, cross-chain compatibility has become a rigid demand.

Tokens on different public chains need to be related to each other. For example, tokens from different public chains can create trading pools in DEX, participate in market making, stake or deposit tokens to other public chains for loans or participate in mining.

However, BTC, as the king of crypto, and the coin with the strongest consensus, highest value, and strongest recognition, does not support smart contracts, making it impossible to establish DEX or participate in deposit loans on the BTC network. So, undoubtedly, to make BTC a cross-chain asset is the strongest rigid demand in the DeFi ecosystem.

Current situation: risk and efficiency

How to build a cross-chain BTC?

The essence of BTC is the data in the decentralized ledger on the BTC blockchain, so only BTC on the BTC network can be recognized by popular consensus.

It is not possible to transfer BTC directly to other public chains. The essence of cross-chain BTC is to lock the BTC on the BTC network and then mint an equal amount of coins on other public chains. The BTC on the BTC chain is native BTC, and the BTC issued by cross-chain minting is cross-chain BTC, or you can call it BTC-pegged token.

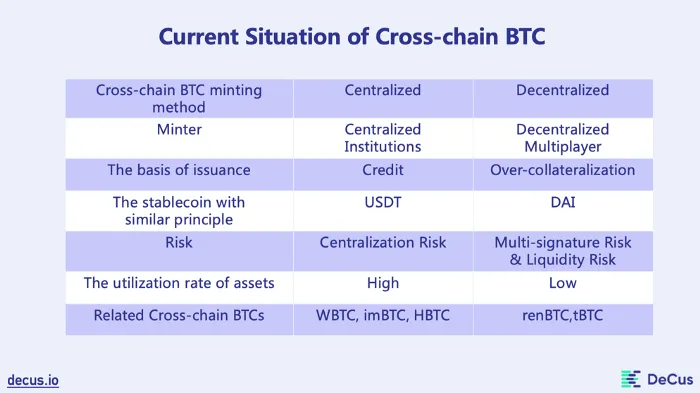

•Centralized cross-chain minting

In the minting process of the cross-chain BTC, the custody of the native BTC is crucial. With centralized minting, a single institution is responsible for holding the users’ native BTC and issuing cross-chain BTC.

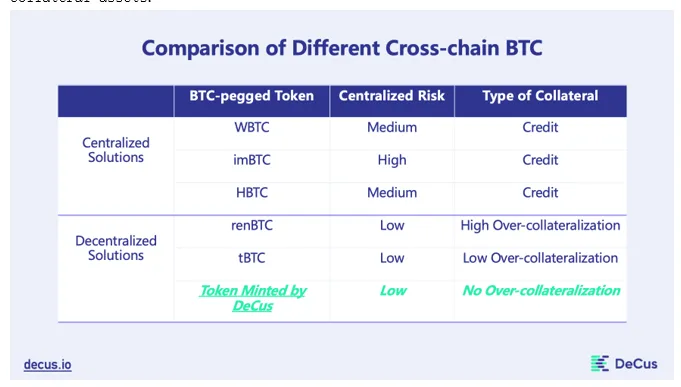

WBTC, imBTC, and HBTC are such centralized minted cross-chain BTC:

➔ WBTC is a cross-chain BTC jointly issued by Kyber, Ren and BitGo.

➔ imBTC is a cross-chain BTC issued by Tokenlon (a decentralized exchange).

➔ HBTC is a cross-chain BTC issued by the Huobi Exchange.

•Decentralized cross-chain minting

Decentralized minting requires participation by multiple people, in a decentralized way, for the custody of native BTC and cross-chain BTC minting.

renBTC and tBTC are such decentralized minted cross-chain BTC:

➔ renBTC performs BTC cross-chain minting and native BTC custody through the RenVM protocol.

➔ tBTC performs BTC cross-chain minting and native BTC custody through multiple signatures.

Centralized risk of cross-chain BTC

The risk of BTC cross-chain lies in the custody of the native BTC. After all, native BTC is the real BTC.

Centralized minting means the issuance of the cross-chain BTC is carried out by a single institution (usually a centralized institution), and the basis of issuance is credit.

WBTC is issued on the basis of the credit of Kyber, Ren, and BitGo; imBTC is issued on the basis of the credit of Tokenlon; HBTC is issued on the basis of the credit of the Huobi platform. Therefore, cross-chain BTC issued by centralized minting is essentially a credit currency. This mechanism is similar to USDT.

Since it is a credit currency, it is naturally exposed to credit risks:

1.The risk of running away. If the centralized custodian embezzles the user’s native BTC, the consequences would be disastrous. Of course, the creditworthiness of these large institutions is still very high, but the loss would be extremely high if it really happens, although the probability of it happening may be considered to be low.

2.The risk of misappropriation of funds. The native BTC pledged by users who want to get cross-chain BTC is kept by a single institution (i.e custodian). If it misappropriates the user’s native BTC, the user will not be able to redeem his or her BTC if the platform’s operation is not good. Similar to the previous example, these institutions and platforms are more creditworthy, so the probability of this happening is relatively low, but the capital at risk is still high.

3.The risk of regulation. Remember when people were unable to make withdrawals from OKEX last year? The person in charge of OKex’s private key was taken away due to regulations, and as a result, users could not withdraw their money. Although most centralized minted coins are also executed across the chain through smart contracts, the custody of native BTC is ultimately centralized. Even if it is held using multiple signatures, 3 signatures are still centralized after all. This risk has a great degree of probability to occur.

4.The risk of value manipulation. Centralized minters have the opportunity to mint a larger number of cross-chain coins on the basis of the number of native BTC locked. This will lead to an inflated quantity of BTC in the market, which on the one hand affects the price of BTC, and on the other hand, the inflated cross-chain BTC can manipulate the market in the cross-chain ecosystem. USDT may do the same thing. The risk of losses from this is hidden and the probability of occurrence is not large, after all, cross-chain BTC is different from USDT, and the quantity of native BTC is visible on the chain. Also, the market will be sensitive to such behavior.

5.The risk of being attacked. With centralized minting, the custody of funds is more centralized, so there is the possibility of being attacked. Although WBTC keeps native BTC in cold wallets, there will always be a portion of BTC in hot wallets in order to meet the redemption demand of users, so it will still be exposed to the risk of being attacked. In addition to wallets, centralized minting is performed by a small number of minters for cross-chain procedures, and once attacked, users’ cross-chain needs may not be met for a short time, or they may even lose their funds. This risk should be temporary and small in scope, and the losses would not be too much, but the probability of occurrence is high.

Decentralization risk of BTC cross-chain

1.Risk of multiple signatures

tBTC has some randomness in managing users’ native BTC. When a user sends a cross-chain request, the tBTC system randomly assigns 3 minters (i.e., multi-signers) to generate a multi-signature address to accept the user’s native BTC. Only when all 3 minters (i.e., multi-signers) have signed can the native BTC in this multi-signer address be transferred.

The problem arises if several minters (i.e., multi-signers) join forces to act criminally together. If they are randomly assigned to the same group, they can take the native BTC that belongs to the user. Not only that, in the tBTC multi-signer mechanism, if a minter (i.e., multi-signer) has a problem, or if the network is blocked, or if the program crashes, or if there is a malicious attack, the signature would be delayed, then the user’s request may be locked, and it cannot be executed.

2.Liquidity risk

Although renBTC and tBTC are almost free from centralization risks, they pose volatility risks because they are collateralized by REN and ETH when they build cross-chain BTC.

For example, on May 19 of this year, when the price of coins collectively dived and the price of ETH and REN took a plunge, the total market value of REN tokens was once lower than the total value of the native BTC placed in custody. The over-collateralization that was used to secure the system no longer existed. At this point, for the minters of renBTC, giving up the collateralized REN and taking possession of the native BTC could have been more profitable. Although renBTC is decentralized, all the minters could ‘coincidentally’ choose to use such a strategy when the price of ren falls, and then the cross-chain users will suffer huge losses.

Capital efficiency issues

Decentralized cross-chain minting is still risky, so the existing decentralized cross-chain BTC minting solutions required collateral issuance, to be precise — over-collateralization. This principle is similar to DAI.

As with DAI minting, building a decentralized cross-chain BTC requires over-collateralization. In the process of decentralized cross-chain minting, financial collateral is required from the minters to prevent them from committing fraud. For every 1 renBTC minted, the minters need to pledge ren tokens worth ≥ 3BTC, and for every tBTC minted, the minters need to pledge ETH worth ≥1.5BTC.

The problem here is the capital efficiency issue. In order to build cross-chain BTC, too much capital has to be pledged, resulting in inefficient capital utilization.

After comparison, we found that the two forms of cross-chain BTC have their own advantages and disadvantages. Centralized cross-chain minting has higher risk, but also higher efficiency; while decentralized cross-chain minting has lower risk of the “single point of failure”, but also has the risk in multiple signatures, the risk in liquidity when the price of the collateral coin falls, and lower capital utilization efficiency.

Innovation: DeCus and eBTC

DeCus: Background and Strengths

DeCus is a highly capital-efficient cross-chain custody platform dedicated to bringing Bitcoin and other assets into other public chains so that they can participate in the DeFi ecosystem of major public chains. According to the public information, DeCus has received investments from several institutions or communities, including Conflux, SevenX, DODO, dForce Labs, FBG Capital, Parallel ventures, and MCDEX. At the top of the list is Conflux.

The exact members of the team are not disclosed due to regulatory reasons in China. However, according to the DeCus official website and DeCus’ community’s confirmation, the core technical team of DeCus comes from the Tsinghua Yao family. The technical model of DeCus is derived from the paper of Dr. Yang Guang, the research director of Conflux, which is published in arXiv, and the paper is about a secure and efficient hosting model.

eBTC: Secure and Efficient

eBTC is the first product of the DeCus system, a decentralized cross-chain BTC issued on the Ethereum network. eBTC has better security and higher efficiency of capital utilization compared with previous cross-chain BTCs. This is in line with the theme of Dr. Yang Guang’s thesis — security and efficiency.

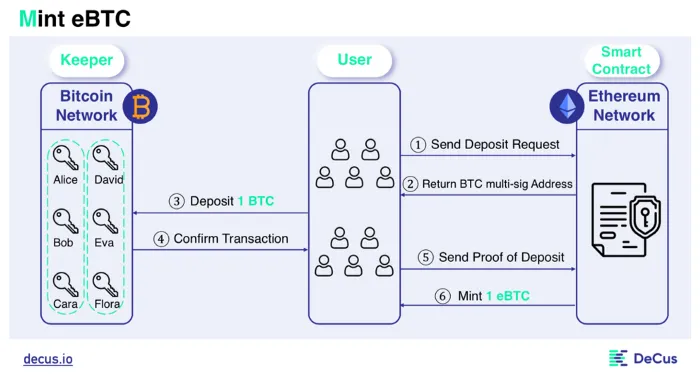

Decentralized cross-chain minting

First of all, eBTC is a cross-chain BTC minted in a decentralized way. The following diagram is the description of the eBTC cross-chain process on the DeCus official website.

A number of custodians hold the multiple signature addresses in a decentralized manner, and it needs more than one-half of the signatures to execute a transfer request. Accepting cross-chain requests, minting coins, and sending eBTC are then executed by a smart contract deployed on the Ethereum network.

The minting is carried out by the smart contract, and multiple people hold the user’s native BTC in a decentralized manner, therefore eBTC is virtually free of the centralization risks discussed earlier.

BTC as collateral

As you can see, minting is executed through smart contracts in the cross-chain process, and there is no centralization risk. Besides, the native BTC transferred by users is held by a group of custodians who are randomly selected, which is the key feature to eBTC with decentralized minting.

To act as an eBTC custodian, BTC must be pledged into the system as collateral, and if the custodian tries to abuse his position, his collateralized BTC will be confiscated.

Multiple signatures

DeCus holds native BTC in groups by means of multiple signatures, and only when more than one-half of the custodians sign can the BTC be dominated.

Assume that there are 6 custodians holding native BTC in groups of 3, with each group sharing custody of multi-signature addresses. By having multiple signatures to keep the native BTC in their addresses, only 2 signatures can execute the transfer, and if only 1 person signs, the number of signatures is less than one-half, so nothing can be transferred, which means if only 1 person abuses the system, it cannot affect the DeCus system security at all.

BTC custodian overlap grouping

What if there are 2 people teaming up to commit fraud?

DeCus has designed a clever decentralized technical model for eBTC — overlapping grouping. To facilitate record keeping, the 6 custodians are represented by ABCDEF in groups of 3, and each custodian can overlap to join a different group. Thus, these 6 individuals would form 20 groupings like this:

ABC ABD ABE ABF

ACD ACE ACF

ADE ADF

AEF

BCD BCE BCF

BDE BDF

BEF

CDE CDF

CEF

DEF

Assuming that 2 of these 6 custodians, AB, team up to commit fraud, then only the group in which both are involved can be controlled. That is, the 4 groups ABC ABD ABE ABF will be attacked by the duo teaming up, which means that only the multi-signature addresses kept by these 4 groups will be influenced.

When accepting cross-chain requests, the smart contract will assign a multi-signature address to the user based on the BTC custody situation of each grouping, which will eventually keep the number of BTC in custody of each custodian group equal.

Assuming that each group keeps the same amount of BTC, then when A and B join forces to commit fraud, they can dominate 4 of the 20 groups, i.e., 1/5 of the native BTC will be stolen by A and B joining forces. However, don’t forget that A and B as custodians have also pledge BTC as collateral. There are 6 custodians in total, and the BTC collateralized by the AB duo accounts for 1/3 but only 1/5 of the BTC get stolen.

To put it in more detail, if there is a total of 30 BTC in the custody pool, then AB teamed up to steal 30/5 = 6 BTC. So, in order to prevent A and B from working together, the two of them can’t collateralize less than 6 BTC, so the total collateralized assets of the 6 custodians can’t be less than 18 BTC.

Thus, we see that 18 or more BTC are collateralized and 30 BTC are held in custody, i.e. 30 eBTC are issued. The collateralization rate is ≥ 60%, which is much smaller than the collateralization rate of renBTC and eBTC.

In fact, there are not actually only 6 custodians in the DeCus system. Using the previous method, let’s calculate the safe collateralization rate when the total number of custodians increase.

If there are 9 custodians, with 3 people in a group, there will be a total of 84 groups, if 2 people work together to commit fraud, they can control 7 groups and steal 7/84 of the BTC in custody, and the collateralized assets of these two are 2/9. This requires a secured collateralization rate of ≥ 37.5%.

If there are 50 custodians, with 3 people in a group, there will be a total of 19,600 groups, if 2 people work together to commit fraud, they can control 48 groups and steal 48/19,600 BTC in custody, and the collateral assets of these two people account for 2/50, so the required security collateralization rate ≥ 6.13%.

Of course, in the DeCus system, the number of BTC under the custody of each grouping cannot be exactly equal, so the actual collateralization rate of the DeCus system will be somewhat higher than that calculated by the model. But what is certain is that the more custodians there are, the lower the security collateralization rate will be.

Obviously, when there are enough custodians, it is possible to increase the group capacity, not necessarily having 3 people in a group, but groups of 5, 7, or more. According to the official information published by DeCus, the collateralization rate of DeCus can be as low as 20%.

So, we see that eBTC has a lower collateral rate and higher efficiency of capital utilization while still ensuring security.

Questions and Outlook

I have studied the DeCus model. The design of this model has an assumption that each multi-signature group keeps an equal amount of BTC. In reality, it is impossible for each group to have an equal number of BTC in their custody. This requires the smart contract to assign the custodian groups when it receives a cross-chain request from a user and tries to keep the number of BTC in each group as equal as possible. If there is a large cross-chain request, my guess is that the user needs to transfer money to multiple multi-signature addresses. So, where is the list of BTC addresses maintained by these multi-signature groups kept? On a centralized server or written to the Ethereum blockchain? If DeCus runs an Ethernet virtual machine, the security is higher, otherwise, there is still the possibility of it being attacked when assigning custodian groups to cross-chain users.

Of course, with the technical strength of the Tsinghua Yao family, it is highly likely that I am overthinking this. But all in all, I believe that DeCus also needs a code security audit to specifically confirm the level of security. If the DeCus code security audit is passed, DeCus will be a very cleverly designed cross-chain system, and eBTC will definitely have a place in the Ethereum ecosystem.

Conclusion

The DeCus system can be understood as a cross-chain protocol, and a stable coin system pegged to BTC. In the DeFi segment, after experiencing hot spots such as lending platforms, algorithmic stable coins, aggregated DeFi, and liquidity mining, can cross-chain DeFi or pegged assets trigger a new round of hot spots?

This question is currently unanswered. However, cross-chain BTC will definitely be an essential and important part of the DeFi ecosystem. Compared with other cross-chain BTC, the design of eBTC has some obvious advantages.

Compared to centralized cross-chain BTCs like WBTC, imBTC, and HBTC, renBTC and tBTC are minted in a decentralized way across chains, reducing the risk of centralization.

However, the over-collateralization of renBTC and tBTC makes the cross-chain minting process more inefficient in terms of capital utilization and has a liquidity risk when the price of the collateralized coins falls.

DeCus System’s eBTC, again, is decentralized cross-chain minting. The use of BTC as collateral, therefore, eliminates the liquidity risk created by fluctuations in collateral assets.

Its biggest innovation is the use of overlapping groupings for multiple signatures to hold native BTC, thus reducing the collateral rate and increasing the efficiency of capital utilization while ensuring security.

The lower collateral rate will attract more investors to compete for DeCus custodians and participate in eBTC minting, so eBTC may have stronger competitiveness in the Ethereum DeFi ecosystem. In turn, higher capital utilization will eventually bring value back to the DeFi market. People who participate in minting can use more funds for buying coins, market making, and other scenarios, thus gaining more profit opportunities.